PE , PS , PVC Prices Rise While PP Tabs Dip

Prices of PE and PS rose in August, and PVC prices were set to move up this month, while PP prices did the reverse.

Prices of PE and PS rose in August, and PVC prices were set to move up this month, while PP prices did the reverse. The spot polyolefins market firmed up in early August with spot PE and PP prices each gaining 1¢/lb, as supplies of both were generally limited, explains Michael Greenberg, CEO of The Plastics Exchange in Chicago. The pricing scenario diverges from there, at least for now: In the case of PE, suppliers were aiming to implement a 3-5¢/lb August price hike and similar increases this month, based on the tight supply situation and firm ethylene monomer prices, whereas PP prices were poised to drop 1-2¢/lb along with that of propylene monomer.

Rising feedstock costs played a key role in reversing the downtrend in PS and PVC prices, abetted in the case of the PVC by revived export markets. That’s the view of purchasing consultants at Resin Technology, Inc. (RTi), Fort Worth, Texas.

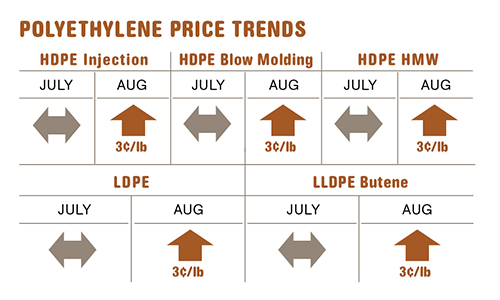

PE PRICES RISE, BUT HOW FAR?

After a sharp decline in the second quarter and a steady July, PE prices appear to be heading up. August contract prices were expected to move up, as most suppliers issued Aug. 1 increases of 5¢/lb, while one dissenter trimmed its hike to 3¢/lb, and grades for some applications were hard to get. Suppliers also issued increases from 3¢ to 5¢ for Sept. 1, but the outcome is questionable.

Domestic demand for PE is flat or up slightly. Ethylene monomer prices have been pretty flat and are not at all a factor in higher PE tabs. Barring any catastrophic event that would affect production, ethylene supply is said to be ample and monomer prices are projected to continue flat-to-down.

Mike Burns, v.p. of PE for RTi, says what made the August 3¢ hike a “shoo-in” was the fact that suppliers’ inventory had dwindled or was being shipped at discounted prices to China and other Asian countries willing to stock up on a good buy. These factors swiftly tightened domestic PE supply. Butene LLDPE and HDPE blow molding grades are reportedly the tightest materials.

But as for the pending September increases, Burns believes demand and feedstock prices are unlikely to support another hike and that suppliers’ inventories will soon increase. Greenberg ventures that the most suppliers will achieve is full implementation of the August 5¢ increase.

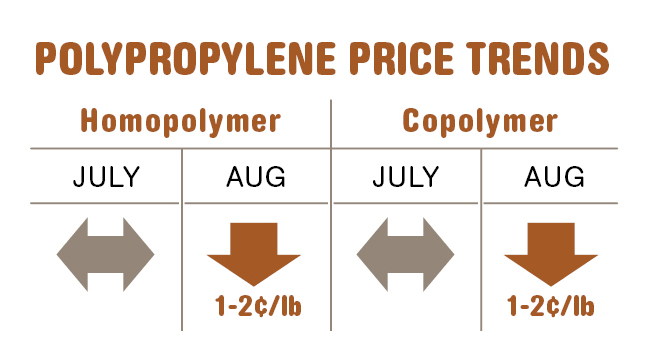

PP PRICES TAKE A SMALL DIP

Polypropylene contract prices dropped 25.5¢/lb in the second quarter and held steady in July, following parallel moves in monomer contracts. Greenberg thinks August PP and monomer contracts will both slide 1-2¢, but that may be a short-lived situation.

According to Robin Chesshier, RTi’s director of client services for PP, suppliers were sold out for the month of August. Material was scarce in secondary markets early in August as well.

Greenberg says July’s domestic PP sales were brisk for the second straight month. He adds that suppliers were able to draw down their inventories to the lowest level since January 2010. Greenberg ventures that with market supply and demand now back in balance—or even a bit undersupplied—some PP suppliers will aim to expand their margins and will look for ways to move away from monomer-plus contracts. “Contract selling prices would potentially float, based on market conditions, as is the case in PE.”

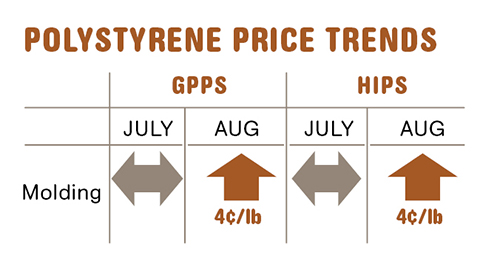

PS PRICES PUSHED UP BY FEEDSTOCKS

Polystyrene prices were moving up last month as the three major North American suppliers sought Aug. 1 increases of 10¢/lb, driven largely by a spike in spot benzene prices. By mid-August, it appeared that 4¢ to 5¢ was sticking, though benzene prices were already retreating, notes Stacy Shelly, RTi’s director of business development for engineering resins, PS, and PVC.

July saw spot benzene prices reaching an all-time high of $5.15/gal at one point. By mid-August, spot benzene had retreated to around $4.30, with forward prices trading around $4.15. Meanwhile, August benzene contracts settled 30¢/gal higher. The benzene hike plus the 3¢/lb increase in July ethylene contracts raised the cost of making PS by 4¢/lb. July styrene monomer contracts were expected to settle 3.5¢ to 4¢/lb higher; while August contract price nominations called for increases of as much as 8¢/lb, Shelly expected the final contract settlements to come in significantly lower.

Domestic PS demand spiked at the end of July, largely due to prebuying in anticipation of price hikes. Shelly cautions that although “true” demand remains soft for now, planned or unplanned plant outages could strain supplies if demand picks up for real. For example, last month’s force majeure at Styrolution’s billion-lb Sarnia, Ont., monomer plant followed an unplanned shutdown and resulted in the company restricting orders for styrene monomer to 75% and PS to 80% of historical usage last month. Meanwhile, Styrolution quickly restarted another monomer plant in Texas with slightly more capacity, which had been down for planned maintenance.

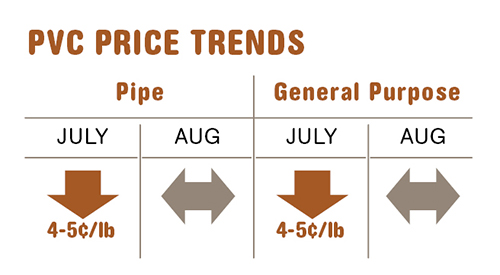

PVC PRICES SET TO RISE

PVC prices stayed flat last month, having dropped a total of nearly 10¢/lb since May. Suppliers called for an increase of 5¢/lb for Sept. 1, but at least one supplier has split it into 3¢ for Sept. 1 and 2¢ for Oct. 1.

Expect to swallow at most 2¢ or 3¢ of all that, says Mark Kallman, director of client services for engineering resins and PVC at RTi. Key factors that halted the price slide of recent months included rising feedstock costs. July ethylene contract prices moved up 3¢/lb and another 1¢ to 2¢ rise was expected last month. Chlorine prices also gained 1¢/lb. These increases boost the cost of making PVC by nearly 3¢/lb. Another factor was a sudden rally in exports in July and August, while domestic demand remained flat.

Related Content

Fundamentals of Polyethylene – Part 5: Metallocenes

How the development of new catalysts—notably metallocenes—paved the way for the development of material grades never before possible.

Read More

The Fundamentals of Polyethylene – Part 2: Density and Molecular Weight

PE properties can be adjusted either by changing the molecular weight or by altering the density. While this increases the possible combinations of properties, it also requires that the specification for the material be precise.

Read More

Fundamentals of Polyethylene – Part 6: PE Performance

Don’t assume you know everything there is to know about PE because it’s been around so long. Here is yet another example of how the performance of PE is influenced by molecular weight and density.

Read More

First Quarter Looks Mostly Flat for Resin Prices

Temporary upward blips don't indicate any sustained movement in the near term.

Read MoreRead Next

See Recyclers Close the Loop on Trade Show Production Scrap at NPE2024

A collaboration between show organizer PLASTICS, recycler CPR and size reduction experts WEIMA and Conair recovered and recycled all production scrap at NPE2024.

Read More

Beyond Prototypes: 8 Ways the Plastics Industry Is Using 3D Printing

Plastics processors are finding applications for 3D printing around the plant and across the supply chain. Here are 8 examples to look for at NPE2024.

Read More

People 4.0 – How to Get Buy-In from Your Staff for Industry 4.0 Systems

Implementing a production monitoring system as the foundation of a ‘smart factory’ is about integrating people with new technology as much as it is about integrating machines and computers. Here are tips from a company that has gone through the process.

Read More