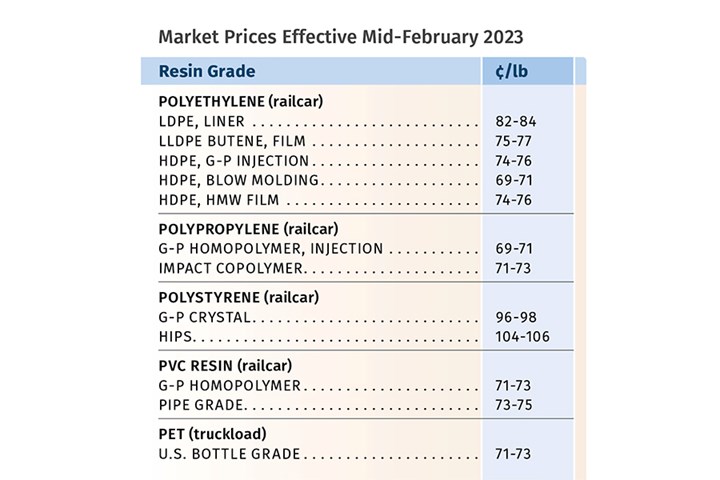

First Quarter Looks Mostly Flat for Resin Prices

Temporary upward blips don't indicate any sustained movement in the near term.

The trend in prices for all five commodity resins in 2023’s first quarter appeared to be flat to slightly higher. Contributing factors included slowed demand (despite dramatically throttled resin production rates), unusual weather-related events and, in some cases, volatile prices of key feedstocks. The direction of prices very much depends on how domestic and global demand shapes up for the second quarter.

These are the views of purchasing consultants from Resin Technology, Inc. (RTi), senior analysts from Houston-based PetroChemWire (PCW), CEO Michael Greenberg of The Plastics Exchange, and Scott Newell, executive v.p. polyolefins at distributor/compounder Spartan Polymers.

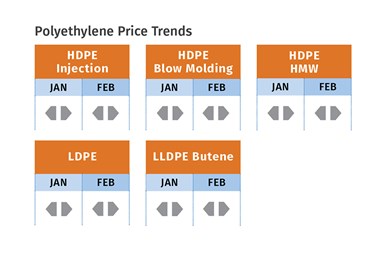

Flat PE Pricing Ahead?

Polyethylene prices in January, were expected to be a roll over from December, but industry reports confirmed that suppliers implemented increases of 3¢/lb increase. In addition to cutting their January scheduled price increases from 5¢ to 8¢/lb down to the 3¢/lb, they then issued additional price hikes for February on the order of 3¢ to 5¢/lb. That’s how it looked to David Barry, PCW’s associate director for PE, PP, and PS; Robin Chesshier, RTi’s v.p. of PE, PS, and nylon 6 markets; and The Plastic Exchange’s Greenberg.

Going into February, RTi’s Chesshier ventured that PE prices could stay flat, barring a major production disruption. “The market is still very depressed in most segments. December was one the worst months, prompting operating rates to fall to the low 70s percentile, the lowest since the 2009 financial crisis.” Moreover, these sources noted the impact of new capacity from Shell, Nova, and Baystar coming on stream, most likely in second quarter. Meanwhile, processors and end users were reported to have a lot of finished goods on hand.

Despite the impact of severe storms that raked the Houston area in late January, PCW’s Barry noted that spot-market buyers believed any tightening of supply would be temporary, with new capacity coming on stream and existing operating rates so low. An exception was likely to be HDPE supply, as Ineos Polyolefins issued a force majeure in late January due to a direct tornado hit, and expected it to take several weeks to restart HDPE and PP production at La Porte, Texas.

Going into February, The Plastic Exchange’s Greenberg reported that while most spot PE prime and off-grade prices held firm, only very limited numbers of prime PE railcars were available. “Reduced production and record exports have drawn producers’ collective PE inventories to their lowest levels since October 2021,” he stated.

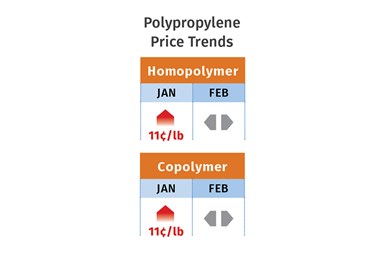

PP Price Move Only a Blip

Polypropylene prices in January moved up by 11¢/lb, in step with propylene monomer, which settled at 43¢/lb. Some further price increase for monomer was possible for February but this month is likely to be flat to lower, according to PCW’s Barry, Spartan Polymers’ Newell, and The Plastic Exchange’s Greenberg. Several suppliers had aimed for a January PP hike of 3¢/lb in addition to any monomer change; going into February, one supplier issued a 6¢/lb non-monomer price hike.

These non-monomer increases appeared unlikely to take hold, and market observers generally concur that PP prices will likely return to being linked solely to the monomer’s price trajectory. Said Spartan Polymers’ Newell, “I see virtually zero chance of a supplier margin gain.” He noted that recent PP price movements were all driven by monomer supply due to planned and unplanned shutdowns and delayed startups. Both he and Barry expected a transition in pricing this month, as monomer was expected to rebalance and then decline in price, with PP to follow. Both stressed that PP prices will need to be on parity with global PP prices. Barry characterized PP spot availability as scarce, with customers having little incentive to rush ahead with orders. In fact, there were reports of order delays for the first time in quite a while.

Greenberg cited the revision by the American Chemistry Council (ACC) to its preliminary December data, which showed PP exports even higher than initially reported — the second highest in seven years. In contrast, domestic sales were even lower — the lowest since March 2013. PP inventories dropped an additional 60 million lb, to more than 300 million lb below the September peak, and entered January at the lowest level in 16 months. “After overproducing and squandering away their wide margins earned on the back of a series of weather-related force majeures in 2021, PP producers have exhibited production discipline the past four months,” reported Greenberg.

How PP demand shapes up will be the key to future prices, according to these sources, along with the impact of new resin and monomer supplies coming on stream — Heartland Polymers and ExxonMobil with new PP capacity, and Heartland and Enterprise with propylene monomer units.

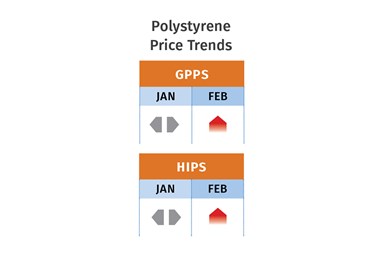

PS Prices Mostly Flat

Polystyrene prices in January held even once again, but some upward movement hovered on the horizon for February and March, according to PCW’s Barry and RTi’s Chesshier. This was attributed solely to volatile benzene prices, since demand was poor and operating rates had dropped below 50%, with lower-priced imports yet another factor.

Two suppliers announced increases of 3¢/lb and 5¢/lb — the latter lining up with the 47¢/gal increase in February benzene contract prices of $3.58/gal, according to PCW’s Barry. Going into February, the implied styrene cost based on a 30% ethylene/70% benzene spot formula was at 42.3¢/lb, up nearly 6¢/lb from late December.

Still, both sources anticipated that PS prices would be flat to only slightly higher in February and March. Chesshier noted that despite costlier benzene, prices of other feedstocks — ethylene, butadiene and styrene monomer — were flat to lower. PS demand fell even more dramatically than had been expected, which led to very low production rates, according to Chesshier, who expected PS prices this month to be flat, barring a major disruption of feedstock production or an upward swing in demand.

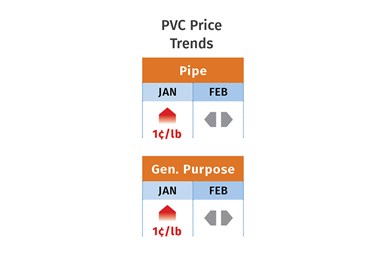

PVC Prices Flat to Slightly Higher

PVC prices in January moved up a bit, generally 1¢/lb, despite suppliers’ announced 6¢/lb increases. February was largely expected to be flat to modestly higher, while suppliers were aiming for a new 4¢lb increase, according to Mark Kallman, RTi’s v.p. of PVC and engineering resins, and PCW senior editor Donna Todd.

Kallman noted that the January increase was a “defensive” move as suppliers tried to stop the price slide. While they had great export activity in December, domestic demand continued to slump, leading to PVC resin operating rates below 70%. He attributed the 1¢ increase in January to higher export prices.

PCW’s Todd reported that suppliers were “anxious” to get back at least some of the 42¢/lb they lost during the second half of 2022. But she reported that buyers saw this year’s two first-quarter price initiatives as “overly ambitious” in view of slack demand demand. “They felt that producers would have been better served by leaving January flat and announcing 3¢/lb increases for February and March, with the possibility for more price hikes in early second quarter,” she said.

PET Prices Down, Up, Flat

PET prices dropped 3¢ to 4¢/lb in December, then moved up 1¢ to 2¢/lb in January, to be followed most likely by flat pricing in February and March. This activity was driven by feedstock costs, particularly paraxylene, according to RTi’s Kallman. “Fluctuation of paraxylene prices started with the late December freeze in Texas, which curtailed production for a time,” he said. Kallman characterized domestic demand as still soft, with plenty of competitively priced imports arriving, although they started to slow due to the slump in domestic demand.

Related Content

The Effects of Time on Polymers

Last month we briefly discussed the influence of temperature on the mechanical properties of polymers and reviewed some of the structural considerations that govern these effects.

Read More

Prices for All Volume Resins Head Down at End of 2023

Flat-to-downward trajectory for at least this month.

Read More

Part 3: The World of Molding Thermosets

Thermosets were the prevalent material in the early history of plastics, but were soon overtaken by thermoplastics in injection molding applications.

Read More

The Effects of Stress on Polymers

Previously we have discussed the effects of temperature and time on the long-term behavior of polymers. Now let's take a look at stress.

Read MoreRead Next

Making the Circular Economy a Reality

Driven by brand owner demands and new worldwide legislation, the entire supply chain is working toward the shift to circularity, with some evidence the circular economy has already begun.

Read More

Beyond Prototypes: 8 Ways the Plastics Industry Is Using 3D Printing

Plastics processors are finding applications for 3D printing around the plant and across the supply chain. Here are 8 examples to look for at NPE2024.

Read More