Contraction Accelerates for Third Month

Index has been trending down since last March.

.JPG;width=70;height=70;mode=crop;format=webp)

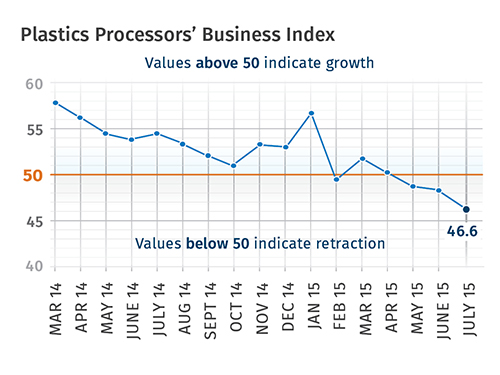

With a reading of 46.6, Gardner’s Plastics Processors’ Business Index contracted for the third month in a row. The index has trended lower since March 2014, except for a brief spurt of accelerating growth from October 2014 to January 2015. In July, the index was at its lowest level since December 2012.

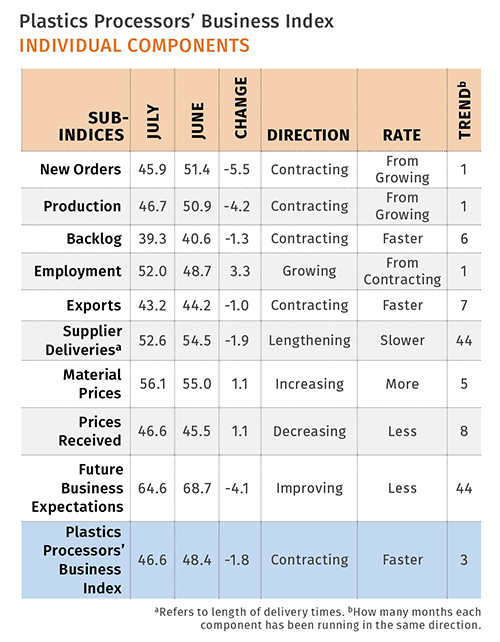

New orders contracted for the first time since October 2013, and the index fell to its lowest level since December 2012. Production contracted for the first time in 31 months. The drop in the production index has been sharp in 2015; it’s also at its lowest level since December 2012.

The backlog index has followed the pattern of the new orders index, moving generally lower since March 2014. It has contracted every month since February. The downtrend in backlogs indicates that capacity utilization will decline into 2016.

Employment increased for the first time since March, but employment tends to be a lagging economic indicator. Just like the new orders and backlog indices, the exports index has trended down since March 2014. Supplier deliveries lengthened at their slowest rate since January 2014, which indicates that slack in the supply chain has increased.

Material prices have increased at an accelerating rate for five months in a row. But oil prices have started falling again, which could limit future material price increases. Prices received have contracted every month since December 2014. Generally, prices received have been decreasing at an accelerating rate. Future business expectations have fallen significantly since December 2014. In July, the index was at its lowest level since November 2012.

Plants with more than 250 employees grew modestly in July. They have expanded in three of the last five months. Facilities with 100-249 employees contracted for the first time since November 2014. Companies with 50-99 employees contracted for the second time in three months. Processors with 20-49 employees have contracted for three consecutive months. In July, they contracted at their fastest rate since December 2012. Processors with 1-19 employees have contracted in every month but one since May 2014.

Every region contracted in July. The West has contracted for four months in a row. Future capital spending plans improved from last month but were still about 66% of their historical average in July. Compared with a year ago, future spending plans have contracted at least 21% in nine of the last 11 months.

Related Content

-

Processing Megatrends Drive New Product Developments at NPE2024

It’s all about sustainability and the circular economy, and it will be on display in Orlando across all the major processes. But there will be plenty to see in automation, AI and machine learning as well.

-

Multilayer Solutions to Challenges in Blow Molding with PCR

For extrusion blow molders, challenges of price and availability of postconsumer recycled resins can be addressed with a variety of multilayer technologies, which also offer solutions to issues with color, processability, mechanical properties and chemical migration in PCR materials.

-

At NPE, Cypet to Show Latest Achievements in Large PET Containers

Maker of one-stage ISBM machines will show off new sizes and styles of handled and stackable PET containers, including novel interlocking products.