Backlogs Surge as Production Deficit Widens

September results show accelerating backlog activity on decelerating production.

.jpg;width=70;height=70;mode=crop;format=webp)

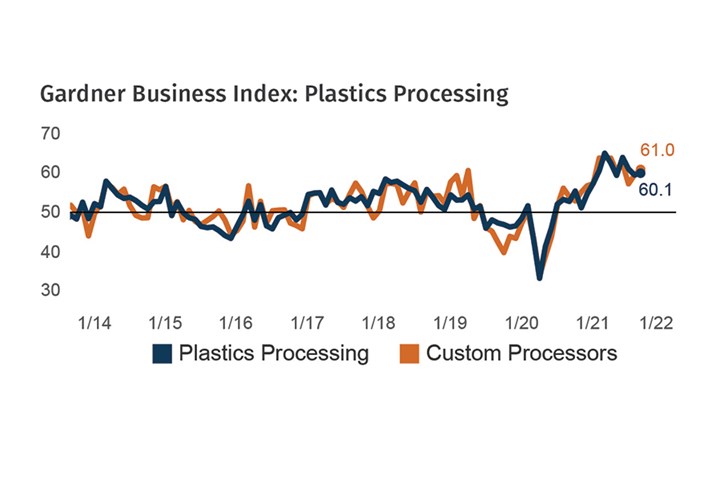

The Gardner Business Index (GBI): Plastics Processing increased modestly in September to close at 60.1. The expansion in overall activity resulted from elevated backlog activity, especially among custom processors surveyed. This was followed by quickening expansion in the readings for total new orders and supplier deliveries. Employment activity slowed for a third consecutive month; the latest reading indicated that payrolls were little better than in August.

FIG 1 The Index registered a slight gain in September as expanding activity in backlogs, supplier deliveries and new orders offset lackluster readings for employment and exports.

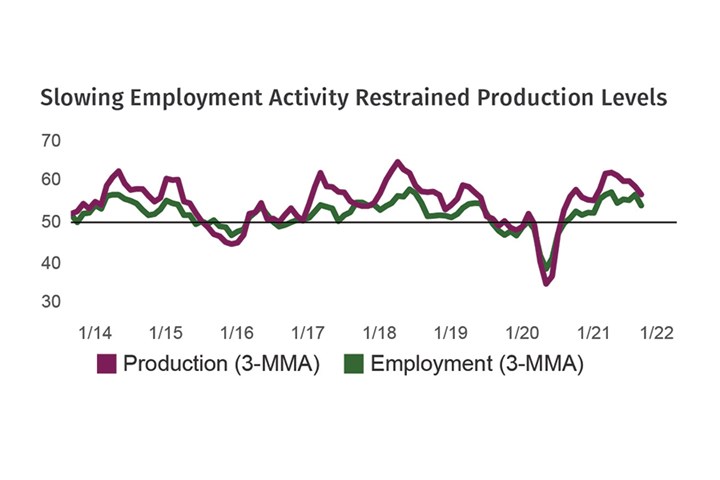

The third quarter brought the hindrance of a sparse labor force into sharp focus for plastics processors. In the four-month period ending September, employment activity went from near all-time highs—signaling strong new hiring—to a stall. This labor deficit coupled with the industry’s ongoing supply-chain problems weighed heavily on production activity, which again reported underwhelming results in September.

FIG 2 The third quarter of 2021 witnessed a dramatic change in employment activity. Simultaneous supply-chain and employment challenges have constricted production and thus inflated backlogs.

This combination of events extended the industry’s “production deficit,” measured as the vertical gap between total new orders and production readings. Measured over the history of the Index, September’s deficit was the highest reported by the industry since the peak of the last business cycle in January 2018.

EDITOR’S NOTE: Finding reliable and relevant data to help guide your business is always important, but especially so during challenging economic times. For this reason, the GBI Plastics Processing and Custom Processing Indices serve as a great tool for making data-driven decisions. Thank you to everyone who has previously completed GBI surveys. Your participation helped increased response counts by 15% in 2020, making the GBI better than ever because of your involvement. Thank you for your time and efforts and for trusting us to provide you with the latest industry and business insights both in the past and in the future.

If you are a North American plastics processor and would like to participate in this research, click here to begin the process by subscribing free to Plastics Technology magazine.

ABOUT THE AUTHOR: Michael Guckes is chief economist and director of analytics for Gardner Intelligence, a division of Gardner Business Media, Cincinnati. He has performed economic analysis, modeling, and forecasting work for more than 20 years among a wide range of industries. He received his BA in political science and economics from Kenyon College and his MBA from Ohio State University. Contact: (513) 527-8800; mguckes@gardnerweb.com.

Related Content

-

Plastics Processing Activity Drops in November

The drop in plastics activity appears to be driven by a return to accelerated contraction for three closely connected components — new orders, production and backlog.

-

Plastics Processing Continued Contraction in April

Despite some index components accelerating and others leveling off, April spelled contraction for overall plastics processing activity.

-

Processing Megatrends Drive New Product Developments at NPE2024

It’s all about sustainability and the circular economy, and it will be on display in Orlando across all the major processes. But there will be plenty to see in automation, AI and machine learning as well.